Net present value calculation explained for business owners. Learn the Time Value of Money, how to determine your discount rate, and step-by-step formulas to evaluate major investments.

BT

Bizcalc Team

·May 15, 2026

Imagine you are the CEO of a growing manufacturing company. Your lead engineer comes to your office and pitches a massive project: "If we spend $500,000 today to upgrade our assembly line, I guarantee it will generate $150,000 in pure cash profit every year for the next five years."

You do the quick mental math. $150,000 a year for 5 years equals $750,000 in total returns.

You invest $500,000, and you get back $750,000. That is a $250,000 profit. It sounds like an absolute no-brainer, right? You should sign the check immediately.

Wrong.

If you make multi-million dollar business decisions using that kind of simplistic, back-of-the-napkin math, you will eventually bankrupt your company. The critical flaw in that basic calculation is that it completely ignores the most fundamental law of corporate finance: The Time Value of Money.

A dollar you receive five years from now is not worth the same as a dollar sitting in your bank account today. To accurately evaluate whether an investment is actually going to make you richer, you cannot simply add up future cash flows. You must "discount" those future dollars back to what they are worth right now, at this exact moment.

This financial translation process is known as Net Present Value (NPV).

In this comprehensive guide, you will find the net present value calculation explained in plain English. We will break down the underlying concept of the time value of money, decipher the complex mathematical formula, guide you on how to choose the correct "discount rate," and provide real-world, step-by-step examples of how to use NPV to make elite, data-driven financial decisions for your business.

📊

NPV Calculator

Skip the complex arithmetic. Enter your initial investment, discount rate, and projected cash flows to instantly calculate Net Present Value and determine if your investment creates real wealth.

1. The Core Concept: The Time Value of Money (TVM)

Before you can calculate Net Present Value, you must fundamentally accept the Time Value of Money (TVM). TVM dictates that money available at the present time is worth more than the identical sum in the future.

If I offer you a choice between receiving $10,000 in cash today or receiving $10,000 exactly one year from today, which do you choose? Every rational human being chooses to take the money today. But why? There are three distinct forces that degrade the value of future money:

A. Inflation (The Silent Thief)

Inflation is the rate at which the general level of prices for goods and services is rising. If inflation averages 3% a year, the $10,000 you receive next year will have 3% less purchasing power than the $10,000 you receive today. It will literally buy you fewer materials, fewer ads, and less labor.

B. Opportunity Cost (The Lost Investment)

If I give you $10,000 today, you can instantly deposit it into a high-yield savings account or an index fund earning 5% interest. By the end of the year, your $10,000 will have grown to $10,500.

If you choose to wait a year to receive the money, you don't just miss out on the $10,000 today; you permanently lose the opportunity to earn that $500 in interest. That $500 is your opportunity cost.

C. Risk (The Uncertainty Principle)

The future is inherently uncertain. If someone promises to pay you $10,000 in five years, there is a risk they might go bankrupt, pass away, or simply refuse to pay. A bird in the hand is worth two in the bush. You demand a premium to accept the risk of waiting for your money.

The Golden Rule of NPV: Because of inflation, opportunity cost, and risk, future cash flows must be mathematically "shrunk" (discounted) before they can be compared to money you are spending today.

*(Note: Don't let the complex math slow down your business decisions. You can instantly run these scenarios using our free NPV Calculator).*

2. What Is Net Present Value (NPV)?

Net Present Value (NPV) is the difference between the present value of cash inflows (the money a project makes you) and the present value of cash outflows (the money you spend to start the project) over a specific period of time.

In simpler terms, NPV calculates exactly how much value a project or investment will add to your company, measured in today's dollars.

The Ultimate Decision Rule

When corporate executives and private equity analysts run an NPV calculation on a potential project, they follow one strict, universally accepted decision rule:

If NPV is Positive (> 0): The investment will generate more value than it costs, even after accounting for the time value of money. Accept the project.

If NPV is Negative (< 0): The investment will result in a net loss of value for the company. The future cash it generates is not enough to justify the initial cost and the waiting period. Reject the project.

If NPV is Exactly Zero (= 0): The investment will perfectly break even. It neither creates nor destroys wealth. You would only accept a zero NPV project if there were massive, unquantifiable strategic benefits (like blocking a competitor from entering a market).

3. The Discount Rate: The Engine of NPV

The single most important variable in an NPV calculation is the Discount Rate.

The discount rate is the interest rate you use to mathematically shrink future cash flows back to their present value. It represents the minimum rate of return your company requires to justify making an investment.

If you use a discount rate of 10%, you are essentially saying, "If this new project cannot generate an annualized return of at least 10%, I am not interested, because I could easily earn 10% by investing my money elsewhere."

But how do you actually choose this number? You don't guess. Companies typically use one of three methods to determine their discount rate:

A. Weighted Average Cost of Capital (WACC)

For established, mid-to-large-sized companies, WACC is the gold standard. WACC calculates exactly how much it costs a company to finance its operations by blending the cost of its debt (interest rates on loans) and the cost of its equity (the return expected by shareholders).

If a company's WACC is 8%, it means it costs them 8% a year just to access capital. Therefore, any new project they take on must use a discount rate of at least 8%, otherwise, the project won't even cover the cost of the money used to fund it.

B. The Hurdle Rate

Many companies simply establish an arbitrary minimum acceptable return, known as a hurdle rate. A CEO might declare, "We are a high-growth tech company. We do not accept any project unless it promises a 15% return." In this case, 15% becomes the discount rate for all NPV calculations across the entire company.

C. Opportunity Cost of Capital

For small businesses and sole proprietors, the discount rate is usually tied to their best alternative safe investment. If a business owner can effortlessly put their cash into a Treasury bond or an S&P 500 index fund and earn a relatively safe 7% per year, they will use 7% as their discount rate. Any new business venture must beat that baseline 7% to be worth the risk and effort.

4. The Formula: Net Present Value Calculation Explained

The mathematical formula for NPV looks intimidating, especially when written in academic financial notation. Let's look at the standard formula and then break it down into plain English.

The Standard NPV Formula:NPV = ∑ [ Rt / (1 + i)^t ] - C0

∑ (Sigma): This simply means "the sum of." You have to run the calculation for every single year of the project, and then add all those years together.

Rt: The net cash flow (money in minus money out) during a specific time period (t).

i: The discount rate (expressed as a decimal, so 10% becomes 0.10).

t: The specific time period (Year 1, Year 2, Year 3, etc.).

C0: The initial capital investment (the money you spend at Year 0 to start the project).

Breaking Down the Present Value (PV) of a Single Year

Before you can calculate Net Present Value, you must understand how to calculate the Present Value (PV) of a single future cash flow.

Let's run a micro-example:

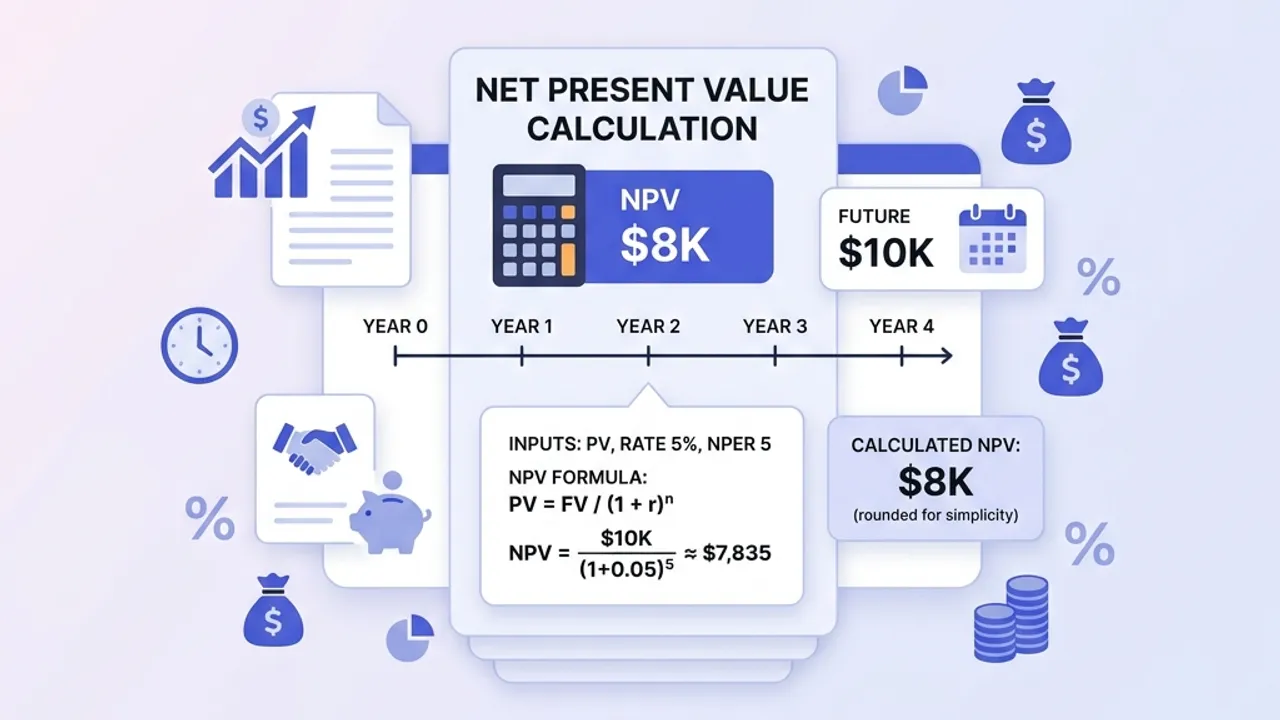

You expect a project to pay you exactly $10,000 at the end of Year 3. Your company's discount rate is 8% (0.08). What is that $10,000 worth to you today?

PV = $10,000 / (1 + 0.08)^3

PV = $10,000 / (1.08)^3

PV = $10,000 / 1.2597

PV = $7,938.39

This calculation proves the time value of money. Because you have to wait three full years to get the money, and because you demand an 8% return, that future $10,000 check is only worth $7,938.39 to your company today.

*(Want to avoid exponential math entirely? The easiest way to get accurate numbers is to plug your projections into an automated NPV Calculator).*

5. A Complete, Step-by-Step Business Example

Let's return to the scenario from the very beginning of this article.

You own a manufacturing company. Your lead engineer wants to buy a new piece of heavy machinery to automate the assembly line.

Initial Cost (C0): $500,000 (spent today, in Year 0).

Projected Returns: The machine will save the company $150,000 in labor costs every year for the next 5 years.

Discount Rate: Your company's WACC is 10% (0.10).

Let's calculate the NPV by discounting each of the 5 years of cash flows, and then subtracting the initial cost.

Year 1

Cash Flow: $150,000

Formula: $150,000 / (1 + 0.10)^1

Present Value: $136,363

Year 2

Cash Flow: $150,000

Formula: $150,000 / (1 + 0.10)^2

Present Value: $123,966

Year 3

Cash Flow: $150,000

Formula: $150,000 / (1 + 0.10)^3

Present Value: $112,697

Year 4

Cash Flow: $150,000

Formula: $150,000 / (1 + 0.10)^4

Present Value: $102,451

Year 5

Cash Flow: $150,000

Formula: $150,000 / (1 + 0.10)^5

Present Value: $93,138

Calculating the Final NPV

⏱️

Payback Period Calculator

Before committing to NPV analysis, check how quickly your investment pays for itself. Use our Payback Period Calculator as a fast first-pass filter.

Now, we sum up the Present Value of all five years of cash flows:

Total Present Value of Cash Inflows = $136,363 + $123,966 + $112,697 + $102,451 + $93,138

Total Present Value = $568,615

Finally, we subtract our initial investment (the money we spent in Year 0):

NPV = Total Present Value - Initial Investment

NPV = $568,615 - $500,000

NPV = $68,615

The Decision

The NPV is $68,615. Because the number is positive, you should accept the project and buy the machine.

Notice how different this reality is from the "back-of-the-napkin" math we did earlier. Initially, it looked like the machine would generate a massive $250,000 profit. However, once we properly accounted for the time value of money and our company's 10% cost of capital, we realized the true value being added to the company is only $68,615 in today's dollars.

If the NPV had come back negative (which would have happened if our discount rate was 16% instead of 10%), we would have rejected the project, realizing that our capital was better spent elsewhere.

6. NPV vs. Other Financial Metrics

While NPV is widely considered the most accurate method for capital budgeting, it is not the only metric executives use. It is crucial to understand how NPV compares to its two biggest rivals: Internal Rate of Return (IRR) and the Payback Period.

A. Internal Rate of Return (IRR) vs. NPV

The Internal Rate of Return (IRR) is closely related to NPV. In fact, IRR is defined as the exact discount rate that forces an investment's NPV to equal exactly zero.

If a project has an IRR of 14%, it means the project generates a 14% annualized return. Executives love IRR because it is expressed as a simple percentage. It is much easier to tell a board of directors, "This project has a 14% return," than it is to say, "This project has an NPV of $42,000."

The Winner: NPV. While IRR is easier to communicate, it has a massive mathematical flaw. It assumes that all future cash flows generated by the project will be perfectly reinvested back into the business at that exact same 14% rate, which is almost never realistic. NPV makes the much safer assumption that cash flows will be reinvested at the company's baseline discount rate. When NPV and IRR give conflicting advice on which project to choose, financial textbooks dictate you must always follow NPV.

B. Payback Period vs. NPV

The Payback Period is the simplest financial metric in existence. It simply asks: "How many years will it take for us to get our initial money back?" If you spend $100,000 and the project generates $25,000 a year, the payback period is 4 years.

The Winner: NPV. The Payback Period is a terrible metric for making major decisions because it ignores two critical things. First, it completely ignores the time value of money (a dollar in Year 4 is treated the same as a dollar in Year 1). Second, it completely ignores all cash flows that occur after the payback period is reached. A project might take 6 years to pay you back, but then generate massive millions in Years 7, 8, and 9. The Payback Period would reject that project; NPV would correctly accept it.

7. The Limitations and Dangers of NPV

While Net Present Value is the gold standard of corporate finance, it is not flawless. Relying on it blindly can lead to catastrophic business decisions if you do not understand its vulnerabilities.

A. The "Garbage In, Garbage Out" Problem

NPV is highly sensitive to the inputs you feed into the formula. The calculation requires you to predict exactly how much cash a project will generate five, ten, or even twenty years into the future.

If your sales team is overly optimistic and projects that a new software product will generate $2 million a year in revenue, your NPV will look incredibly positive. But if the market shifts and the software only generates $500,000 a year, your initial positive NPV was a dangerous illusion. A mathematical formula cannot save you from bad market research.

B. Sensitivity to the Discount Rate

A slight tweak to the discount rate can instantly turn a highly profitable project into a massive loser. If the Federal Reserve raises interest rates, your company's cost of borrowing money increases, which forces your WACC (and your discount rate) to rise.

If you evaluated a 10-year construction project using a 6% discount rate, the NPV might be +$1 Million. If you re-run that exact same project with an 8% discount rate, the NPV might crash to -$500,000. Executives must frequently run "sensitivity analyses" to see how their NPV changes if interest rates fluctuate.

C. It Ignores "Sunk Costs" and Flexibility

Standard NPV assumes a project is a static, binary decision: you either do it or you don't. It fails to account for managerial flexibility.

For example, if you build a new factory and the market crashes after two years, you wouldn't just sit there and absorb the losses for the next eight years as the original NPV model predicted. You would pivot, sell the machinery, or lease the building to a competitor. To account for this flexibility, highly advanced financial analysts use "Real Options Valuation" instead of static NPV.

8. Real-World Applications of NPV

Net Present Value is not just a theoretical concept taught in MBA programs. It is used daily across every major industry to allocate trillions of dollars in capital.

Real Estate Development: A developer wants to build a $50 million apartment complex. They project rental income, maintenance costs, and property taxes for the next 30 years. They discount those cash flows back to today to determine if they should buy the land or walk away.

Mergers and Acquisitions (M&A): When a massive tech company considers buying a smaller startup for $2 Billion, they are running an NPV calculation. They project the startup's future cash flows, discount them back using their corporate WACC, and if the NPV is positive, they execute the buyout.

Software Development: A SaaS company debates spending $200,000 to hire developers to build a new premium feature. They estimate how many current users will upgrade to the premium tier over the next three years, calculate the NPV, and decide if the engineering time is worth the investment.

Final Thoughts on Capital Budgeting

Business is essentially the act of allocating scarce resources. You have a limited amount of cash, a limited amount of engineering talent, and a limited amount of time. You cannot pursue every single good idea that crosses your desk.

Understanding the net present value calculation empowers you to cut through the noise, ignore the vanity metrics, and mathematically prove which projects will actually build wealth for your company, and which projects will quietly destroy it.

Before you sign the check for your next major marketing campaign, equipment purchase, or new hire, map out the cash flows. Determine your required rate of return. Shrink those future dollars back to the present.

If the final number is positive, execute aggressively. If the final number is negative, walk away without looking back.

📊

NPV Calculator

Stop guessing and start calculating. Enter your projected cash flows to instantly determine the true present value of your next investment.

Net Present Value (NPV) is a financial metric that calculates the current value of a future series of cash flows, discounted at a specific rate, minus the initial investment.

Why is the discount rate important in NPV?

The discount rate accounts for the time value of money and project risk. A higher discount rate reduces the present value of future cash flows, making a project look less attractive.

What does a positive NPV mean?

A positive NPV indicates that the projected earnings (in present dollars) exceed the anticipated costs. Generally, an investment with a positive NPV will be profitable and should be accepted.

What is the difference between NPV and ROI?

ROI measures the total percentage return of an investment, but ignores the time value of money. NPV accounts for inflation and the cost of capital over time, providing a more accurate dollar value.

Can NPV be negative?

Yes, a negative NPV means the project is expected to lose money (or earn less than your required discount rate) and should typically be rejected.

#net present value calculation explained#NPV formula#time value of money#discount rate#capital budgeting#business valuation