The current ratio calculation explained in simple terms. Learn how to measure your company's short-term liquidity, interpret the results, and avoid a cash flow crisis.

BT

Bizcalc Team

·May 15, 2026

Imagine your business is a high-performance sports car. Your revenue is the top speed, and your profit margin is the fuel efficiency. Both of these metrics are incredibly important to track.

However, there is one metric that matters far more than speed or efficiency: Do you actually have enough fuel in the tank to make it to the next gas station?

If you run out of fuel on the highway, it doesn't matter how fast your car is capable of going. The journey is over. In the business world, running out of "fuel" means running out of short-term cash. A company can be wildly profitable on paper, generating millions of dollars in future contracts, and still go completely bankrupt in a matter of weeks if it cannot pay its immediate bills.

To prevent this catastrophic scenario, financial analysts, banks, and elite business owners rely on a fundamental liquidity metric: The Current Ratio.

In this comprehensive guide, you will find the current ratio calculation explained from the ground up. We will break down exactly what goes into the formula, provide real-world examples, contrast it against stricter liquidity tests, and show you exactly how to interpret the numbers to bulletproof your business against a cash flow crisis.

Table of Contents

1. What Is the Current Ratio?

The Current Ratio is a liquidity metric that measures a company's ability to pay off all of its short-term obligations (debts and payables due within one year) using its short-term assets (cash, inventory, and receivables that can be converted to cash within one year).

It is the ultimate test of your company's immediate financial survival.

When a commercial bank reviews your loan application, or a major vendor decides whether to offer you "Net 60" payment terms, the Current Ratio is usually the very first metric they check. They are asking one simple, brutal question: "If every single one of this company's short-term creditors demanded their money today, could the company liquidate its current assets and pay everyone off?"

If the answer is yes, you are considered "liquid." If the answer is no, you are operating on a razor's edge.

📊

Current Ratio Calculator

Instantly check your company's liquidity health. Plug in your current assets and liabilities to see if you are operating in the safe zone.

2. The Formula: Current Ratio Calculation Explained

The mathematics behind the Current Ratio are incredibly straightforward. You only need two numbers, both of which are readily available at the top of your company's balance sheet.

The Formula:Current Ratio = Current Assets / Current Liabilities

While the division is easy, the complexity lies in understanding exactly what accounting items qualify as "Current." If you accidentally include a long-term asset in this calculation, your ratio will be wildly inaccurate, giving you a false sense of security.

Understanding "Current Assets"

A Current Asset is any resource owned by the company that is either already cash or is realistically expected to be converted into cash within the next 12 months.

Cash and Cash Equivalents: The money currently sitting in your checking and savings accounts, plus highly liquid short-term investments like Treasury bills.

Accounts Receivable (AR): The money your customers owe you for products or services you have already delivered. (Assuming they will pay you within the year).

Inventory: The raw materials and finished goods sitting in your warehouse waiting to be sold.

Prepaid Expenses: Things you have already paid for in advance, like a 12-month commercial insurance premium.

Crucially, this does NOT include Long-Term Assets. You cannot include the value of your office building, your manufacturing equipment, or your company vehicles. While those things have massive value, you cannot easily sell a warehouse by next Friday to make payroll. They are not liquid.

Understanding "Current Liabilities"

A Current Liability is any debt or obligation that your company legally must pay within the next 12 months.

Accounts Payable (AP): The money you owe to your suppliers, vendors, and contractors.

Short-Term Debt: Credit card balances, lines of credit, or short-term bridge loans.

Current Portion of Long-Term Debt: If you have a 10-year commercial mortgage, the 10-year total is not a current liability. However, the exact amount of principal you must pay this year is a current liability.

Accrued Liabilities: Taxes owed to the government, or wages you owe to your employees but haven't paid out yet.

3. A Step-by-Step Calculation Example

Let's look at a practical example to see how the Current Ratio calculation works in the real world. We will analyze a fictional retail business called Summit Outdoor Gear.

The CEO of Summit wants to know if the company is healthy enough to survive an upcoming slow season. She pulls the latest balance sheet:

Summit's Current Assets:

Cash in the bank: $50,000

Accounts Receivable: $30,000

Inventory (tents, boots, jackets): $120,000

Total Current Assets = $200,000

Summit's Current Liabilities:

Accounts Payable (owed to suppliers): $60,000

Short-term business loan: $25,000

Taxes owed: $15,000

Total Current Liabilities = $100,000

The Calculation:

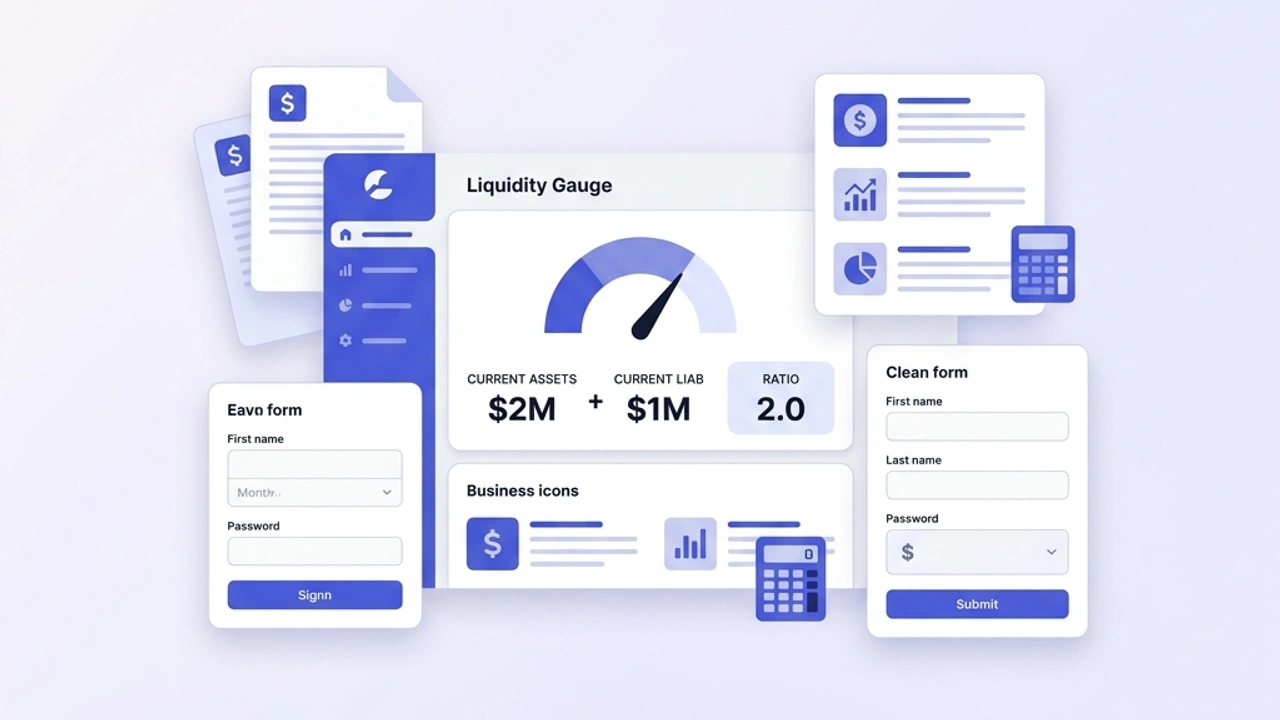

Current Ratio = $200,000 / $100,000

Current Ratio = 2.0

This means Summit Outdoor Gear has exactly $2.00 in liquid assets for every $1.00 of short-term debt it owes. The company is in fantastic financial shape and can easily weather a slow season.

🏦

Working Capital Calculator

Beyond ratios, calculate the exact dollar amount of working capital you have available to fund your day-to-day operations.

Calculating the number is the easy part. The true skill of an elite business owner lies in interpreting what the number actually means for the future of the company.

Let's break down the three distinct "zones" your ratio can fall into.

The Danger Zone: A Ratio Below 1.0 (< 1.0)

If your Current Ratio is below 1.0, your Current Liabilities exceed your Current Assets. This is a massive red flag. It means that if all your bills came due tomorrow, you would not have enough cash (even after selling all your inventory and collecting all your debts) to pay them.

A ratio of 0.8 means you only have 80 cents for every dollar you owe. If a company stays below 1.0 for an extended period, it is almost certainly heading toward bankruptcy or a severe restructuring. You must immediately inject cash into the business or radically restructure your debt.

The Sweet Spot: A Ratio Between 1.5 and 2.5

For the vast majority of standard businesses, a Current Ratio between 1.5 and 2.5 is considered the ultimate sweet spot.

It proves to banks and investors that you have a thick, comfortable cushion of liquidity. You can effortlessly handle unexpected emergencies—like a major client refusing to pay an invoice, or a sudden supply chain disruption—without missing your own payroll. You are financially secure.

The Warning Sign: A Ratio Above 3.0 (> 3.0)

You might logically assume that if a ratio of 2.0 is good, a ratio of 5.0 must be incredible. This is actually a misconception.

While a shockingly high Current Ratio guarantees you won't go bankrupt, it usually indicates that the CEO is highly inefficient with capital. If your ratio is 5.0, it means you are hoarding massive amounts of cash in a checking account doing nothing, or you have massive piles of unsold inventory rotting in a warehouse.

That excess cash shouldn't be sitting idle; it should be heavily reinvested into marketing, hiring new talent, or acquiring competitors to drive long-term growth.

5. The Fatal Flaw: Why the Current Ratio Can Lie to You

While the Current Ratio is the most popular liquidity metric in the world, it has one massive, potentially fatal flaw: It assumes all inventory can be instantly sold for cash.

Let's go back to our example of Summit Outdoor Gear. Their Current Ratio was a phenomenal 2.0. But let's look closer at their $200,000 in Current Assets.

Only $50,000 was actual cash.

A massive $120,000 was tied up in inventory.

What happens if there is an abnormally warm winter, and absolutely nobody wants to buy their heavy winter coats? That $120,000 in inventory is functionally worthless in the short term. The company cannot pay the bank with winter coats.

If Summit cannot sell that inventory, their "true" liquid assets drop to just $80,000 (Cash + AR). Against their $100,000 in liabilities, they are suddenly operating at a terrifying 0.8 ratio, and they are in severe danger of defaulting on their loans.

The Solution: The Quick Ratio (The Acid Test)

Because inventory is notoriously difficult to liquidate quickly during a crisis, strict financial analysts prefer to use a much harsher metric called the Quick Ratio (also known as the Acid-Test Ratio).

The Quick Ratio strips inventory out of the equation entirely, forcing the company to prove it can survive using only its absolute most liquid assets.

The Formula:Quick Ratio = (Cash + Accounts Receivable) / Current Liabilities

If a company has a Current Ratio of 2.0, but a Quick Ratio of 0.5, it means the business is dangerously bloated with unsold inventory. A healthy business should aim for a Quick Ratio of at least 1.0.

6. Industry Benchmarks: What Is Normal?

Just like the Debt-to-Equity ratio, what is considered a "good" Current Ratio fluctuates wildly depending on the industry you operate in. You cannot compare a grocery store to a software company.

Retail and Grocery (Acceptable Ratio: 0.8 to 1.2)

You will frequently see massive, highly successful retail chains operating with a Current Ratio slightly below 1.0. How do they survive?

Retailers have incredibly fast inventory turnover. When you buy groceries, you pay with a credit card immediately. The grocery store gets the cash instantly. However, the grocery store negotiates "Net 60" or "Net 90" terms with the farmers and suppliers who provided the food. Because they collect cash from customers weeks before they have to pay their suppliers, they can safely operate with a very low Current Ratio.

Technology and SaaS (Acceptable Ratio: 1.5 to 3.0+)

Software as a Service (SaaS) companies typically have incredibly high Current Ratios.

They have absolutely zero physical inventory. Their current assets are almost entirely composed of pure cash in the bank, raised from venture capitalists or generated from highly profitable subscription revenues. Because they lack the fast cash-conversion cycles of a retail store, they need a higher ratio to feel secure.

Manufacturing (Acceptable Ratio: 1.5 to 2.5)

Manufacturers have massive amounts of capital tied up in raw materials, work-in-progress inventory, and finished goods. Because the process of turning raw steel into a sold product takes months, they require a very healthy Current Ratio cushion to ensure they can pay their factory workers while they wait for their inventory to finally sell.

7. Four Strategies to Improve a Dangerous Current Ratio

If you run your numbers and discover you are stuck in the danger zone (< 1.0), you must take immediate, aggressive action before a single unexpected expense destroys your business.

Here are four strategies to rapidly improve your liquidity:

A. Accelerate Your Accounts Receivable

If you have thousands of dollars trapped in outstanding invoices, you are effectively acting as a free bank for your clients. You must speed up collections.

Require a 50% upfront deposit before starting any new work.

Shorten your payment terms from "Net 30" to "Due on Receipt."

Offer a 2% discount if clients pay their invoice within 5 days.

B. Renegotiate with Your Suppliers (Stretch Payables)

While you want to speed up the money coming in, you want to slow down the money going out. Call your most trusted vendors and ask to extend your payment terms from 30 days to 60 days. This allows you to keep the cash in your own bank account longer, instantly improving your Current Ratio at the end of the month.

C. Restructure Short-Term Debt into Long-Term Debt

Remember, the Current Ratio formula divides your assets by your Current Liabilities (debt due within 12 months). Long-term debt does not count against your Current Ratio.

If you have a massive $50,000 credit card balance that is crushing your liquidity, go to a bank and take out a 5-year term loan to pay off the credit card. You haven't eliminated the debt, but you have shifted it from a "Current Liability" to a "Long-Term Liability," instantly rescuing your Current Ratio and freeing up your immediate cash flow.

D. Liquidate Dead Inventory

If your warehouse is full of old products that haven't sold in a year, they are dragging down your capital efficiency. Run a massive clearance sale and sell that dead inventory at cost, or even at a slight loss. While it hurts your profit margin for the month, it instantly converts a slow-moving asset into liquid cash, directly improving your Quick Ratio and giving you the capital you need to survive.

Final Thoughts on Cash Management

Profit is vanity. Cash flow is sanity.

You can build the greatest product in the world, generate massive sales numbers, and still fail if you do not fiercely protect your liquidity.

Understanding the current ratio calculation explained in this guide is your first line of defense. By consistently monitoring your Current Assets and Current Liabilities, you transform from a reactive owner constantly stressed about making payroll, into a proactive CEO who knows exactly how much fuel is left in the tank.

Never fly blind. Make it a mandatory part of your month-end accounting process to check your liquidity.

🏦

Free Current Ratio Calculator

Take control of your cash flow right now. Plug your balance sheet numbers into our interactive calculator to instantly measure your financial health.

The current ratio is a liquidity metric that measures a company's ability to pay its short-term obligations (due within one year) using its short-term assets.

What is considered a good current ratio?

A current ratio between 1.5 and 2.0 is generally considered healthy. It indicates the business has enough assets to comfortably cover its short-term liabilities without holding excess idle cash.

What does a current ratio of less than 1 mean?

A ratio below 1 means the company has more short-term debt than short-term assets, which could indicate potential liquidity problems or difficulty paying upcoming bills.

How does the current ratio differ from the quick ratio?

The current ratio includes all current assets (like inventory). The quick ratio is stricter and excludes inventory, focusing only on the most liquid assets like cash and accounts receivable.

How can a business improve its current ratio?

A business can improve its current ratio by paying down short-term debt, negotiating longer payment terms with suppliers, or converting short-term debt into long-term loans.

#current ratio calculation explained#liquidity ratio#current assets#current liabilities#financial health#cash flow management