What Is Loan Amortization and How to Read an Amortization Schedule

Understand loan amortization and how to read an amortization schedule. Learn the formula, see worked examples, and know exactly where your payments go each month.

BT

Bizcalc Team

·June 15, 2026

When you take out a mortgage, a business loan, a car loan, or any other fixed-term borrowing, your lender provides a repayment structure built on a concept called amortization. Most borrowers make their monthly payments faithfully for years without ever fully understanding what is happening to that money — specifically, how much is reducing their debt and how much is flowing to the lender as interest.

Understanding loan amortization — and being able to read an amortization schedule — is one of the most practically valuable financial skills a business owner, property investor, or individual borrower can develop. It tells you exactly how much of your balance you have paid off at any point, reveals the true cost of your loan in interest, and shows you precisely how extra payments accelerate your debt reduction.

This guide explains the mechanics of loan amortization from the ground up, walks through the underlying formula, presents a full worked example with a complete amortization table, and covers the strategic decisions you can make once you understand how the schedule works.

📋

Amortization Schedule Calculator

Enter your loan amount, interest rate, and term to instantly generate a full month-by-month amortization schedule showing principal, interest, and remaining balance.

Amortization is the process of paying off a debt through scheduled, equal periodic payments over a defined period. With each payment, a portion reduces the outstanding principal (the amount you borrowed) and a portion covers the interest charged for that period.

The defining feature of a fully amortizing loan is that the payment amount remains constant throughout the loan term, yet the split between principal and interest shifts with every payment. In the early stages of a loan, the majority of each payment covers interest. As the balance declines, interest charges shrink and a progressively larger share of each payment goes toward the principal. By the final payment, almost the entire amount is principal.

This shifting dynamic — constant payment, changing composition — is the essence of amortization. It is neither arbitrary nor hidden; it is a mathematically precise result of how interest is calculated on a declining balance.

Key Terminology

Before reading an amortization schedule, it helps to be clear on the terms involved:

Term

Definition

Principal

The original amount borrowed, or the outstanding balance still owed

Interest Rate

The annual percentage rate (APR) charged by the lender

Loan Term

The total length of the loan, usually expressed in months or years

Monthly Payment

The fixed amount paid each period (usually monthly)

Principal Portion

The part of each payment that reduces the outstanding balance

Interest Portion

The part of each payment that covers interest charges for the period

Remaining Balance

The outstanding principal after each payment is applied

Total Interest Paid

The cumulative interest paid over the full life of the loan

The Amortization Formula

The monthly payment on a fully amortizing loan is calculated using the following formula:

M = P × [r(1 + r)^n] ÷ [(1 + r)^n − 1]

Where:

M = Monthly payment

P = Loan principal (amount borrowed)

r = Monthly interest rate = Annual rate ÷ 12 (expressed as a decimal)

n = Total number of payments = Loan term in years × 12

This formula calculates the fixed payment amount that will exactly pay off the loan — principal and all interest — by the final scheduled payment, assuming no missed payments or overpayments.

How Each Period's Interest and Principal Are Calculated

Once you have the monthly payment (M), each period's breakdown is calculated as follows:

Principal = Monthly Payment − Interest for the Period

New balance:

New Balance = Previous Balance − Principal Paid

These three steps are repeated for every payment in the schedule. Because the outstanding balance decreases with each payment, the interest charge also decreases each period — which is why the principal portion grows over time even as the total payment stays fixed.

M = 200,000 × [0.005 × 6.02258] ÷ [6.02258 − 1]

M = 200,000 × 0.030113 ÷ 5.02258

M = 200,000 × 0.005996

M = $1,199.10 per month

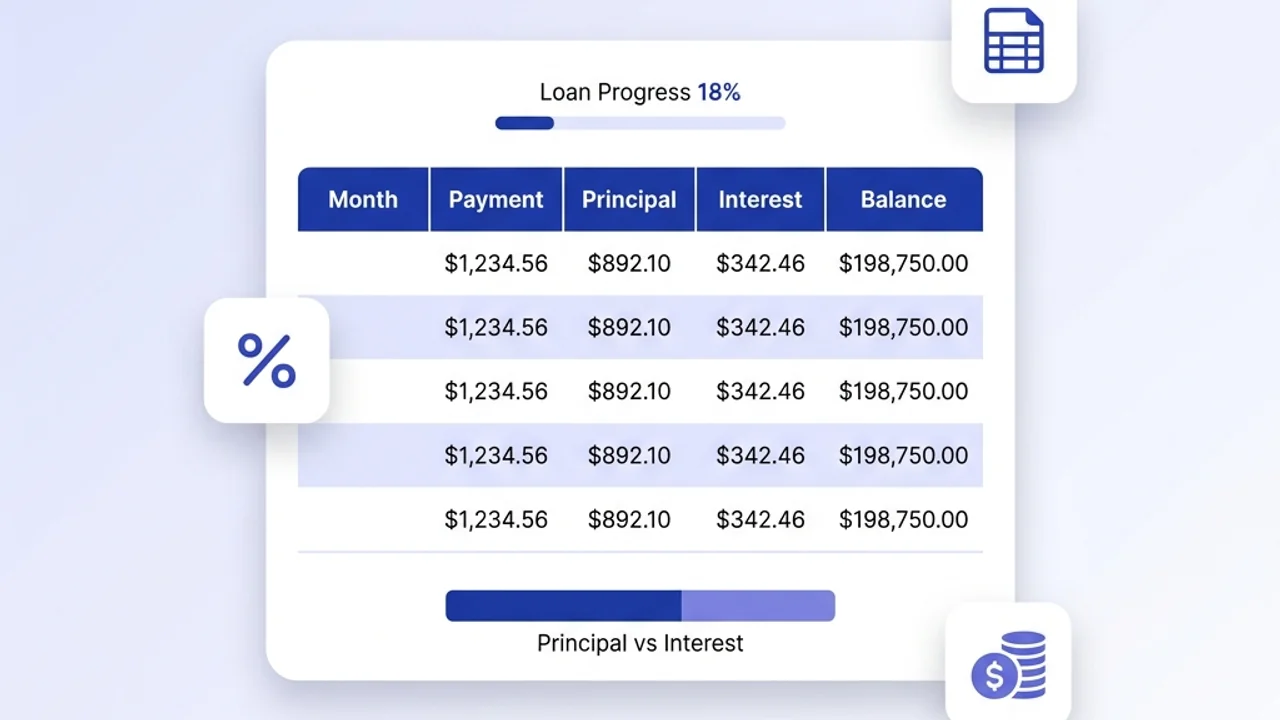

Step 2: Build the First 12 Months of the Amortization Schedule

Month

Opening Balance

Payment

Interest

Principal

Closing Balance

1

$200,000.00

$1,199.10

$1,000.00

$199.10

$199,800.90

2

$199,800.90

$1,199.10

$999.00

$200.10

$199,600.80

3

$199,600.80

$1,199.10

$998.00

$201.10

$199,399.70

4

$199,399.70

$1,199.10

$997.00

$202.10

$199,197.60

5

$199,197.60

$1,199.10

$995.99

$203.11

$198,994.49

6

$198,994.49

$1,199.10

$994.97

$204.13

$198,790.36

7

$198,790.36

$1,199.10

$993.95

$205.15

$198,585.21

8

$198,585.21

$1,199.10

$992.93

$206.17

$198,379.04

9

$198,379.04

$1,199.10

$991.90

$207.20

$198,171.84

10

$198,171.84

$1,199.10

$990.86

$208.24

$197,963.60

11

$197,963.60

$1,199.10

$989.82

$209.28

$197,754.32

12

$197,754.32

$1,199.10

$988.77

$210.33

$197,543.99

After 12 full monthly payments totalling $14,389.20, the balance has reduced by only $2,456.01. The remaining $11,933.19 went entirely to interest. This is the front-loaded nature of amortization made visible.

Key Milestones on This Loan

Milestone

Occurs At

Interest and principal portions are equal

Month ~252 (Year 21)

25% of principal repaid

Month ~121 (Year 10)

50% of principal repaid

Month ~223 (Year 18.6)

Loan fully paid off

Month 360 (Year 30)

Total interest paid over 30 years

$231,676

On a $200,000 loan at 6%, the borrower pays $231,676 in interest — more than the original loan amount — over the full 30-year term. This figure, which the amortization schedule makes completely transparent, is one of the most important numbers any borrower should know before committing to a loan.

📋

Amortization Schedule Calculator

Generate a complete amortization table for any loan amount, rate, and term — and see your total interest cost before you sign.

A standard amortization schedule contains six columns. Here is how to interpret each one:

Column 1: Payment Number (or Month)

The sequential number of each payment, from 1 to the total number of payments. For a 30-year mortgage, this runs from 1 to 360.

Column 2: Opening Balance

The outstanding loan balance at the beginning of the period, before this month's payment is applied. In the first period, this equals the original loan amount. Every subsequent period uses the previous period's closing balance.

Column 3: Payment Amount

The fixed total payment due for the period. This amount stays the same for every row in a standard fixed-rate amortizing loan. For variable-rate loans, this column will change when the rate resets.

Column 4: Interest Portion

The interest charged on the opening balance for this period:

Interest = Opening Balance × Monthly Rate

This figure decreases with every row because the opening balance is always slightly lower than the previous period.

Column 5: Principal Portion

The amount of the payment applied to the outstanding balance:

Principal = Payment − Interest

This figure increases with every row as the interest portion shrinks.

Column 6: Closing Balance

The remaining balance after this payment is applied:

Closing Balance = Opening Balance − Principal Paid

This should reach zero (or very close to it, due to rounding) on the final scheduled payment.

What to Look For When Reading Your Schedule

Total interest cost: Sum the interest column for all rows. This is the true cost of borrowing over the loan's full life.

Your equity position at any point: The original loan amount minus the closing balance at any row is the equity you have built through repayment.

The interest-to-principal crossover point: Find the row where the principal portion first exceeds the interest portion. This is the inflection point of the loan.

The effect of your planned payoff date: If you plan to sell a property or refinance after 7 years, find row 84 and note the closing balance — that is what you will still owe.

How Different Loan Variables Affect the Schedule

1. Interest Rate

The interest rate has a profound impact on both the monthly payment and the total interest paid. Using our $200,000 example with a 30-year term:

Annual Rate

Monthly Payment

Total Interest Paid

Total Cost

4.0%

$954.83

$143,739

$343,739

5.0%

$1,073.64

$186,512

$386,512

6.0%

$1,199.10

$231,676

$431,676

7.0%

$1,330.60

$279,018

$479,018

8.0%

$1,467.53

$328,310

$528,310

Moving from a 4% rate to a 7% rate on a $200,000 mortgage increases the total interest cost by $135,279 — nearly 94% more. The interest rate is by far the most impactful variable in the entire schedule.

2. Loan Term

Extending or shortening the term changes both the monthly payment and the total interest dramatically:

Loan Term

Monthly Payment

Total Interest Paid

Total Cost

10 years

$2,220.41

$66,449

$266,449

15 years

$1,687.71

$103,788

$303,788

20 years

$1,432.86

$143,886

$343,886

25 years

$1,288.60

$186,580

$386,580

30 years

$1,199.10

$231,676

$431,676

(All at 6% annual rate on $200,000)

Choosing a 15-year term over 30 years saves $127,888 in interest — at the cost of a higher monthly payment ($488.61 more per month). For borrowers with sufficient cash flow, the shorter term represents a dramatically better financial outcome.

3. Loan Amount

The monthly payment and total interest scale proportionally with the loan amount. Borrowing $100,000 instead of $200,000 at the same rate and term halves the payment and halves the total interest. This relationship is linear.

The Power of Extra Principal Payments

One of the most useful things an amortization schedule reveals is the disproportionate impact of additional principal payments, particularly early in the loan term.

Example: $500 Extra Payment per Month

Returning to our $200,000 loan at 6% over 30 years:

Scenario

Monthly Payment

Loan Paid Off In

Total Interest Paid

Interest Saved

Standard payments only

$1,199.10

30 years

$231,676

—

+$200/month extra principal

$1,399.10

~24.5 years

$183,220

$48,456

+$500/month extra principal

$1,699.10

~19.5 years

$140,105

$91,571

+$1,000/month extra principal

$2,199.10

~14.5 years

$99,210

$132,466

Adding just $500 per month to the principal payment shortens the loan by 10.5 years and saves over $91,500 in interest. The savings are amplified the earlier the extra payments begin, because they reduce the balance that accumulates interest over subsequent years.

Important: Before making extra payments, always confirm that your loan agreement does not include an early repayment charge or prepayment penalty. In some jurisdictions and loan types, these fees can reduce or eliminate the financial benefit of overpaying.

Amortization in a Business Context

While amortization is most commonly associated with residential mortgages, the same principles apply to every fixed-term business loan.

Business Term Loans

When a business takes out a term loan to fund equipment, an acquisition, a fit-out, or a working capital need, the lender provides an amortization schedule. Understanding this schedule is essential for:

Cash flow planning: Knowing the exact monthly payment allows accurate cash flow forecasting. The Cash Flow Projection Calculator can incorporate your amortization payments into a full forward-looking cash position.

Debt servicing ratio: Lenders evaluate whether a business can service its debt by comparing loan payments to EBITDA. Use the Debt-to-Equity Calculator to monitor your leverage position over the life of the loan.

Tax deductibility of interest: In most jurisdictions, the interest portion of business loan payments is tax-deductible, while principal repayments are not. The amortization schedule gives you the precise interest figure for each tax period.

True cost of business borrowing: A business evaluating a $500,000 equipment loan at 7% over 7 years will pay approximately $130,000 in interest over the term — a cost that should be weighed against the productivity or revenue gain the equipment generates.

Commercial Real Estate

Commercial property loans typically have shorter amortization periods than residential mortgages (often 20–25 years) and may include balloon payments — a structure where the regular payments are calculated on a 25-year amortization but the full remaining balance is due after 5 or 10 years. Understanding the amortization schedule is critical for planning the balloon payment refinancing.

Vehicle and Equipment Finance

Asset finance for business vehicles or equipment is nearly always structured as a fully amortizing loan. The schedule allows the business to track the loan balance relative to the asset's depreciation — a comparison relevant to both balance sheet management and insurance decisions. Pair this analysis with the Depreciation Calculator to see how your asset value tracks against your outstanding loan balance over time.

Fixed-Rate vs. Variable-Rate Amortization

The amortization schedule described throughout this guide assumes a fixed interest rate — the most straightforward case, where the payment amount and the principal/interest split for each period can be calculated precisely from day one.

Variable-rate (adjustable-rate) loans add complexity. The payment amount changes when the rate resets, requiring the schedule to be recalculated from that point forward using the new rate and the outstanding balance at the time of the reset. Borrowers with variable-rate loans should request an updated amortization schedule each time the rate changes.

Key considerations for variable-rate loans:

The initial schedule is only a projection, not a fixed commitment.

If rates rise significantly, the monthly payment may increase substantially.

Some variable-rate loans are structured with a fixed payment but a variable term — if rates rise, the loan takes longer to pay off rather than the payment increasing.

Amortization vs. Other Loan Structures

Loan Type

How It Works

Amortization Schedule?

Fully Amortizing

Equal payments; both principal and interest paid throughout

Yes — standard schedule

Interest-Only

Payments cover only interest; principal unchanged

No — balance does not decrease

Balloon Loan

Smaller regular payments + large final lump sum

Partial — balance remains at balloon point

Bullet Loan

No regular payments; full principal + interest due at maturity

No

Revolving Credit

Flexible drawdown and repayment; no fixed schedule

No

Most business term loans, mortgages, vehicle loans, and personal loans are fully amortizing. If you are unsure of your loan's structure, the presence of a consistent fixed monthly payment and a declining balance is a strong indicator of full amortization.

Amortization Schedule Checklist

Use this checklist when reviewing an amortization schedule for any loan:

Verify the total payment amount matches what your lender quoted.

Confirm the loan term (number of payments) matches your agreement.

Check the closing balance on the final payment reaches zero (or near zero).

Sum the interest column to see the full lifetime interest cost before you sign.

Identify the interest-principal crossover point to understand when your payments start primarily reducing debt.

Note your balance at key dates — e.g., when you plan to sell, refinance, or have the loan reviewed.

Model the impact of extra payments to quantify interest savings and term reduction.

Confirm prepayment penalty terms before making any additional principal payments.

For business loans, extract the annual interest figures for tax filing purposes.

For variable-rate loans, note the rate review dates and request an updated schedule after each reset.

Final Thoughts

An amortization schedule is one of the most transparent and informative documents in personal or business finance. Far from being a dry table of numbers, it is a complete map of your debt: where it starts, how it declines, where the money goes every month, and exactly when it ends.

The single most important insight most borrowers take from their amortization schedule is the total interest figure — the cumulative cost of borrowing over the full loan term. Seeing that a $200,000 loan at 6% generates $231,676 in interest over 30 years changes how people think about their borrowing decisions, their loan term choices, and the value of making extra principal payments.

Run your own numbers before you borrow, and revisit your schedule regularly as you repay.

💳

Loan Payment Calculator

Compare different loan amounts, rates, and terms side by side to find the structure that best fits your monthly budget and total cost goals.

An amortization schedule is a complete table showing every payment on a loan from the first to the last. For each payment it breaks down how much goes toward reducing the principal balance and how much covers interest, along with the remaining balance after the payment is made.

Why do early loan payments go mostly toward interest?

Because interest is calculated as a percentage of the outstanding balance, and the balance is highest at the start of the loan. As you make payments and reduce the principal, the interest portion of each payment shrinks and the principal portion grows — even though the total payment amount stays the same.

How is the monthly payment on an amortizing loan calculated?

The formula is M = P × [r(1+r)^n] ÷ [(1+r)^n − 1], where M is the monthly payment, P is the loan principal, r is the monthly interest rate (annual rate ÷ 12), and n is the total number of payments. Most online amortization calculators apply this formula automatically.

What happens if I make extra principal payments on an amortizing loan?

Extra principal payments reduce your outstanding balance immediately, which means less interest accrues in subsequent periods. This shortens the overall loan term and reduces the total interest paid over the life of the loan — sometimes significantly. Many lenders allow overpayments without penalty, but always verify the loan terms first.

Is every loan amortizing?

No. Interest-only loans require no principal repayment during the interest-only period, so the balance does not decrease. Balloon loans have smaller regular payments with a large lump-sum payment due at the end. Revolving credit (credit cards, lines of credit) has no fixed repayment schedule. Only fully amortizing loans — such as most mortgages, car loans, and business term loans — follow a set amortization schedule.