Depreciation Methods Explained: Straight-Line vs Declining Balance

Confused by depreciation? Learn how straight-line and declining balance methods work, compare formulas, and find the right option for your business assets.

BT

Bizcalc Team

·June 26, 2026

A manufacturing company spends $100,000 on a heavy-duty packaging system. The machine will help package products for the next ten years, after which it will be sold for scrap metal.

If the company lists the entire $100,000 as an expense in the month of purchase, the profit and loss statement shows a massive loss. The next nine years, meanwhile, show artificially high profit margins because the packaging machine helps generate sales without showing any ongoing cost.

This distortion is why accounting uses depreciation. Depreciation matches the cost of a physical asset to the revenue it helps generate over its useful life.

The choice of depreciation method alters your company's balance sheet, taxable income, and cash flow. Selecting the right approach requires comparing the steady simplicity of the straight-line method against the front-loaded tax benefits of the declining balance method.

📊

Depreciation Calculator

Compare straight-line and declining balance depreciation schedules side-by-side to find the right strategy for your business assets.

Before comparing formulas, you must understand the four key terms that define any depreciation schedule.

1. Cost Basis (Initial Cost)

This is the total cost to acquire the asset and prepare it for operation. It includes the purchase price, delivery charges, installation fees, and testing costs. Your calculations always start with this number.

2. Salvage Value (Residual Value)

This is the estimated value of the asset at the end of its useful life. It represents what you expect to receive when you sell or scrap the asset. Some assets (such as computers) have a salvage value of zero, while others (such as heavy equipment) retain substantial value.

3. Useful Life (Service Life)

This is the period over which the asset is expected to remain productive. Useful life is measured in years. Tax authorities (like the IRS or HMRC) often publish standardized asset class guidelines that dictate the useful life you must use for tax filings.

4. Net Book Value (Carrying Value)

This is the current value of the asset on your balance sheet. It is calculated by subtracting cumulative depreciation from the initial Cost Basis:

Book Value = Cost Basis - Cumulative Depreciation

The asset's book value decreases each year until it matches the salvage value. At that point, depreciation stops.

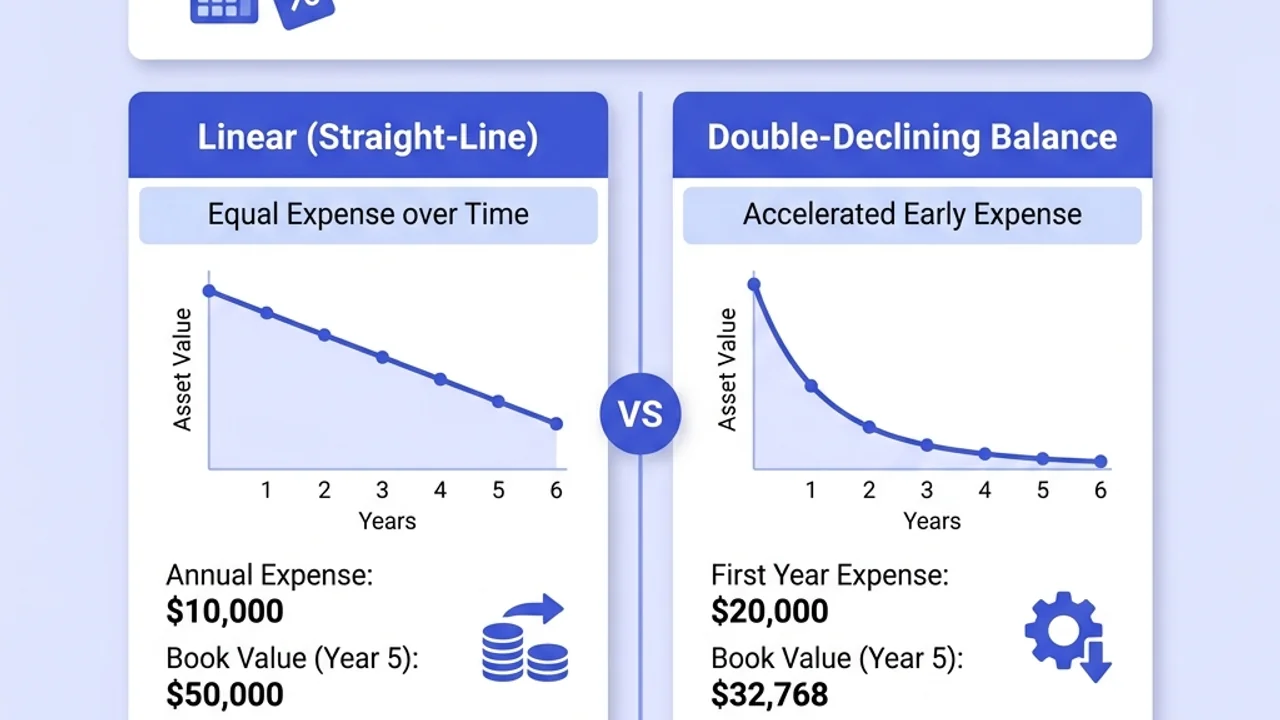

Straight-Line Depreciation: Steady Simplicity

The straight-line method is the most common way to calculate depreciation. It distributes the asset's cost evenly over its useful life.

The Straight-Line Formula

The calculation requires subtracting the salvage value from the cost basis to find the total depreciable cost, then dividing by the useful life.

The declining balance method is an accelerated depreciation system. It calculates a higher depreciation expense in the early years of the asset's life and lower expenses in the later years.

This method reflects the physical reality of many assets. A new commercial delivery van loses a massive portion of its resale value the moment you drive it off the lot. It also requires minimal maintenance early on. In the later years, the van's depreciation slows down, but its maintenance costs rise. Accelerated depreciation keeps total asset ownership costs (depreciation plus maintenance) relatively stable over time.

The Declining Balance Formula

To calculate declining balance depreciation, you apply a constant rate to the asset's beginning book value at the start of each year.

Unlike the straight-line method, you do not subtract the salvage value from the cost basis at the start. Instead, you apply the rate to the full book value, but you must stop the calculation once the book value matches the salvage value.

The most common version is the Double-Declining Balance (DDB) method, which devalues the asset at twice the straight-line rate.

Depreciation Rate = Multiple / Useful Life

For double-declining balance, the multiple is 2:

Double-Declining Rate = 2 / Useful Life

Once you have the rate, calculate the annual expense:

Annual Depreciation = Beginning Book Value * Depreciation Rate

For a $50,000 asset with a 5-year useful life:

Straight-line rate: 1 / 5 = 20% per year

Double-declining rate: 2 * 20% = 40% per year

Year 1 Depreciation: $50,000 * 40% = $20,000

Year 2 beginning book value: $50,000 - $20,000 = $30,000

Year 2 Depreciation: $30,000 * 40% = $12,000

The Salvage Value Floor and the Crossover Rule

Because you calculate declining balance depreciation by multiplying a fraction against a declining balance, the book value will mathematically never reach zero. It also risks dropping below the salvage value.

To manage this, you must apply the salvage value floor rule. You can only depreciate the asset until its book value matches the salvage value. In the final years of the schedule, you must adjust the calculation to a flat amount that brings the book value exactly down to the salvage value, rather than multiplying by the rate.

To ensure the asset is fully depreciated on schedule, businesses often switch from the double-declining balance method to the straight-line method mid-way through the asset's life. The switch occurs in the first year where the straight-line calculation (remaining depreciable cost divided by remaining years) yields a higher expense than the declining balance calculation.

📊

Depreciation Calculator

Generate a complete depreciation schedule showing the exact crossover points and salvage value floors.

Step-by-Step Guide to Comparing Depreciation Methods

Comparing these two methods requires calculating their schedules side-by-side. Follow these steps to map the financial impact of each choice.

Step 1: Collect Asset Parameters

Get the initial purchase price, shipping/setup costs (to establish the Cost Basis), the expected salvage value, and the useful life in years.

Step 2: Build the Straight-Line Schedule

Divide the depreciable cost (Cost minus Salvage Value) by the useful life. Write down this constant annual expense for each year of the term.

Step 3: Build the Declining Balance Schedule

Calculate the accelerated depreciation rate (e.g., 2 divided by useful life). For each year, multiply this rate by the beginning book value to find the expense. Subtract the expense to find the ending book value, which becomes the beginning book value for the next year. Keep an eye on the salvage value floor.

Step 4: Compare Cash Flows and Net Income

Analyse the resulting tables. Look at how the choice of method shapes your annual expenses. Higher early expenses reduce your reported profits but lower your tax liability, preserving cash in the short term.

Detailed Case Studies

These case studies show how the choice of depreciation method impacts your financial metrics.

Case Study A: The Delivery Van

A retail bakery buys a refrigerated delivery van.

Cost Basis: $45,000

Useful Life: 5 Years

Salvage Value: $5,000

Depreciable Cost: $40,000 ($45,000 cost basis minus $5,000 salvage value)

Method 1: Straight-Line Schedule

The straight-line rate is 1 / 5, which equals 20% per year. The annual depreciation expense is $8,000 ($40,000 divided by 5 years).

Year

Beginning Book Value

Depreciation Expense

Cumulative Depreciation

Ending Book Value

Year 1

$45,000

$8,000

$8,000

$37,000

Year 2

$37,000

$8,000

$16,000

$29,000

Year 3

$29,000

$8,000

$24,000

$21,000

Year 4

$21,000

$8,000

$32,000

$13,000

Year 5

$13,000

$8,000

$40,000

$5,000

Method 2: Double-Declining Balance Schedule

The double-declining rate is 2 / 5, which equals 40% per year. We apply this 40% rate to the beginning book value of each year.

Year 1: $45,000 * 40% = $18,000 expense. Ending book value is $27,000.

Year 2: $27,000 * 40% = $10,800 expense. Ending book value is $16,200.

Year 3: $16,200 * 40% = $6,480 expense. Ending book value is $9,720.

Year 4: $9,720 * 40% = $3,888 expense. Ending book value is $5,832.

Year 5: If we apply the 40% rate to the beginning book value of $5,832, the calculated expense is $2,332.80, which would drop the ending book value to $3,499.20. Because the book value cannot drop below the $5,000 salvage value, we limit the Year 5 expense to the exact amount needed to reach the floor: $5,832 - $5,000 = $832.

Year

Beginning Book Value

Depreciation Expense

Cumulative Depreciation

Ending Book Value

Year 1

$45,000

$18,000

$18,000

$27,000

Year 2

$27,000

$10,800

$28,800

$16,200

Year 3

$16,200

$6,480

$35,280

$9,720

Year 4

$9,720

$3,888

$39,168

$5,832

Year 5

$5,832

$832 (Adjusted)

$40,000

$5,000

Comparing the Results

Look at the Year 1 difference. The Double-Declining Balance method matches the rapid real-world devaluation of a new van, recording $18,000 in depreciation compared to only $8,000 under the straight-line method. This $10,000 difference represents an extra deduction that lowers taxable income. By Year 5, both methods have depreciated the van down to its $5,000 salvage value. The difference is the timing of the expense recognition.

Case Study B: Production Machinery (Switchover Analysis)

A manufacturing plant purchases a packaging machine.

Cost Basis: $120,000

Useful Life: 8 Years

Salvage Value: $20,000

Depreciable Cost: $100,000

Double-Declining Rate: 2 / 8 = 25% per year

If we run the double-declining balance calculation without switching, the final years become highly inefficient because the annual expense drops to very low numbers. To prevent this, the company switches to the straight-line method in the year where the straight-line method yields a higher expense.

Let's trace the declining balance schedule:

Year 1: $120,000 * 25% = $30,000. Ending book value: $90,000.

Year 2: $90,000 * 25% = $22,500. Ending book value: $67,500.

Year 3: $67,500 * 25% = $16,875. Ending book value: $50,625.

Year 4: $50,625 * 25% = $12,656. Ending book value: $37,969.

Let's test the crossover point in Year 5:

Remaining depreciable cost: $37,969 book value minus $20,000 salvage value = $17,969.

Remaining useful life: 4 years (Years 5, 6, 7, and 8).

Straight-line calculation on remaining balance: $17,969 / 4 years = $4,492 per year.

If we apply the declining balance expense of $5,340, the book value drops to $16,018, which violates the $20,000 salvage value floor. We must switch to the straight-line method to devalue the remaining $1,358 evenly over the final 2 years:

Year 7 expense: $679. Ending book value: $20,679.

Year 8 expense: $679. Ending book value: $20,000.

This switchover ensures the machine is depreciated down to its exact salvage value on time, avoiding the calculation dead-end of pure declining balance formulas.

Tax and Financial Reporting Implications

The choice of depreciation method is not just an academic exercise. It directly shapes your cash position.

The Tax Shield

Depreciation is a non-cash expense. You do not write a check for depreciation each year, yet it is deducted from your revenues to calculate your taxable income.

A larger depreciation expense in the early years reduces your taxable income, lowering your tax payments. The cash you save on taxes remains in your business bank account, improving liquidity. This cash savings acts as a tax shield.

Because money has time value (a dollar today is worth more than a dollar in the future), front-loading your depreciation deductions using an accelerated method increases the net present value of the cash flows generated by the asset. You can analyze this financial dynamic using the Net Present Value Calculator.

Book vs. Tax Differences

Many jurisdictions allow businesses to use one depreciation method for tax reporting and another for financial reporting.

For Tax Purposes: Businesses often use accelerated depreciation methods to lower their current tax bill.

For Financial Statements: They use the straight-line method to show stable earnings to investors and lenders.

Using two different methods creates a temporary timing difference. The taxes you save today are deferred to the future, recorded on your balance sheet as a deferred tax liability.

Choosing the Right Depreciation Method

To determine which method fits your business, review the operational characteristics of your asset and your financial goals.

Use the Straight-Line Method if:

The asset's productivity remains identical from Year 1 to the final year.

The asset does not face a high risk of technological obsolescence.

You want simple, stable financial reporting for bank loans or investors.

You are depreciating long-term assets like buildings or property.

Use the Declining Balance Method if:

The asset is a vehicle, computer system, or tech device that loses value rapidly.

Maintenance costs are low early on but will rise significantly in the future.

You want to lower your tax liability immediately to preserve operating cash.

You want your balance sheet to match the actual market resale value of the asset.

Summary Checklist for Asset Depreciation

Before setting up your next asset schedule, verify these details:

Confirm the Cost Basis: Check that you have included shipping, installation, and setup fees in the starting cost.

Verify Useful Life Guidelines: Check the official tax authority tables to ensure your useful life estimate matches the required class life.

Establish a Salvage Value: Determine a realistic residual value based on historical sales or scrap rates.

Select Your Method: Decide between straight-line stability and accelerated declining balance tax shields.

Run the Calculations: Use a digital Depreciation Calculator to generate the complete schedules and identify the salvage value floor.

By matching the right depreciation method to each asset type, you preserve cash flow, simplify tax compliance, and maintain a clear picture of your company's net book value.

📊

Depreciation Calculator

Generate print-ready straight-line and double-declining balance tables for your business assets.

What is the primary difference between straight-line and declining balance depreciation?

Straight-line depreciation spreads the asset's cost evenly over its useful life, resulting in an identical expense each year. The declining balance method is an accelerated system that calculates depreciation as a percentage of the asset's remaining book value, resulting in much higher expenses in the early years.

Why do companies choose accelerated depreciation methods over straight-line?

Accelerated methods like double-declining balance provide larger tax deductions in the early years of an asset's life. This early tax savings improves short-term cash flow, allowing businesses to reinvest capital sooner.

Can you depreciate an asset below its salvage value?

No. Regardless of the method you use, the total cumulative depreciation cannot exceed the asset's depreciable cost (initial cost minus salvage value). Under the declining balance method, you must stop depreciating once the asset's book value matches its salvage value.

How does the choice of depreciation method affect financial statements?

Straight-line depreciation keeps expenses stable and reported profits higher in the early years. Declining balance reduces reported profits initially but increases them in the later years of the asset's life, though cash flow is improved early on due to lower tax payments.

Is a company allowed to switch depreciation methods mid-way through an asset's life?

Generally, tax authorities permit a one-time switch from the declining balance method to the straight-line method to ensure the asset is fully depreciated down to its salvage value by the end of its useful life. Changing methods for financial reporting requires proving that the new method better represents the asset's economic utility.