Learn how to calculate PTO accrual step by step. Covers hourly, per-pay-period, and annual accrual methods with examples, accrual rate tables, and cap policies.

BT

Bizcalc Team

·May 24, 2026

Paid Time Off (PTO) is one of the most valued components of any employment package. Employees think about it constantly — tracking their balance, planning holidays around it, and factoring it into their decision to join or leave a company. Yet for many business owners and HR managers, the mechanics of how PTO actually accrues remains surprisingly murky.

Get it wrong, and you face a range of painful consequences: employees with incorrect balances on their pay stubs, compliance violations under local employment law, costly payouts at termination when accrued-but-unused balances are larger than expected, and — perhaps most damaging — a breakdown in employee trust when the numbers don't match what was promised.

This comprehensive guide will show you exactly how to calculate PTO accrual using every major method, with worked examples for each. We will cover hourly accrual, per-pay-period accrual, annual grants, accrual caps, payout policies, and how to build a PTO structure that is both fair to employees and sustainable for your business.

Table of Contents

1. What Is PTO Accrual?

PTO accrual is the process by which employees earn their paid time off gradually over time rather than receiving it all at once at the start of the year. Each hour worked, each pay period completed, or each milestone reached adds a defined increment to the employee's leave balance.

The alternative to accrual is a lump-sum grant — awarding the full year's PTO on January 1st (or on the employee's work anniversary). Both approaches have their place, and we will cover both. But accrual is far more common in organizations with more than a handful of employees, for two main reasons:

Cash flow and liability management: Under accrual, the business's PTO liability builds gradually. Under a lump-sum grant, 100% of the year's liability is created on day one — including for employees who may leave six months later having used their entire allocation.

Fairness: Accrual rewards tenure. An employee who joins on October 1st earns a proportional amount of PTO for the quarter they worked, rather than a full year's allocation they haven't yet earned.

(Want to skip the manual calculation? Our free PTO Accrual Calculator handles all the math — just enter the hours worked and your accrual rate.)

📅

PTO Accrual Calculator

Enter your accrual rate, pay frequency, and hours worked to instantly calculate employee PTO balances and year-end projections.

Before diving into the specific calculation methods, it helps to understand the five variables that appear in virtually every PTO accrual formula:

Variable

Definition

Example

Annual PTO Entitlement

Total days/hours of PTO the employee earns per year

15 days (120 hours)

Working Hours Per Year

Total hours the employee is expected to work annually

2,080 hours (40 hrs/wk × 52 wks)

Accrual Rate

PTO hours earned per hour worked (or per pay period)

0.0577 hrs per hour worked

Hours Worked

Actual hours worked in the current period

80 hours (one biweekly pay period)

Accrual Cap

Maximum PTO balance the employee can hold at any time

1.5× annual entitlement

Every PTO accrual calculation is simply a matter of combining these variables in the right way for your chosen accrual method.

3. Method 1: Hourly Accrual (Most Precise)

Hourly accrual is the most precise and legally defensible method. PTO is earned in direct proportion to every hour worked. This method is especially common for hourly and part-time workers because it automatically adjusts for variable schedules.

The Formula:Accrual Rate = Annual PTO Hours / Annual Working Hours

PTO Earned This Period = Accrual Rate × Hours Worked This Period

Step-by-Step Example

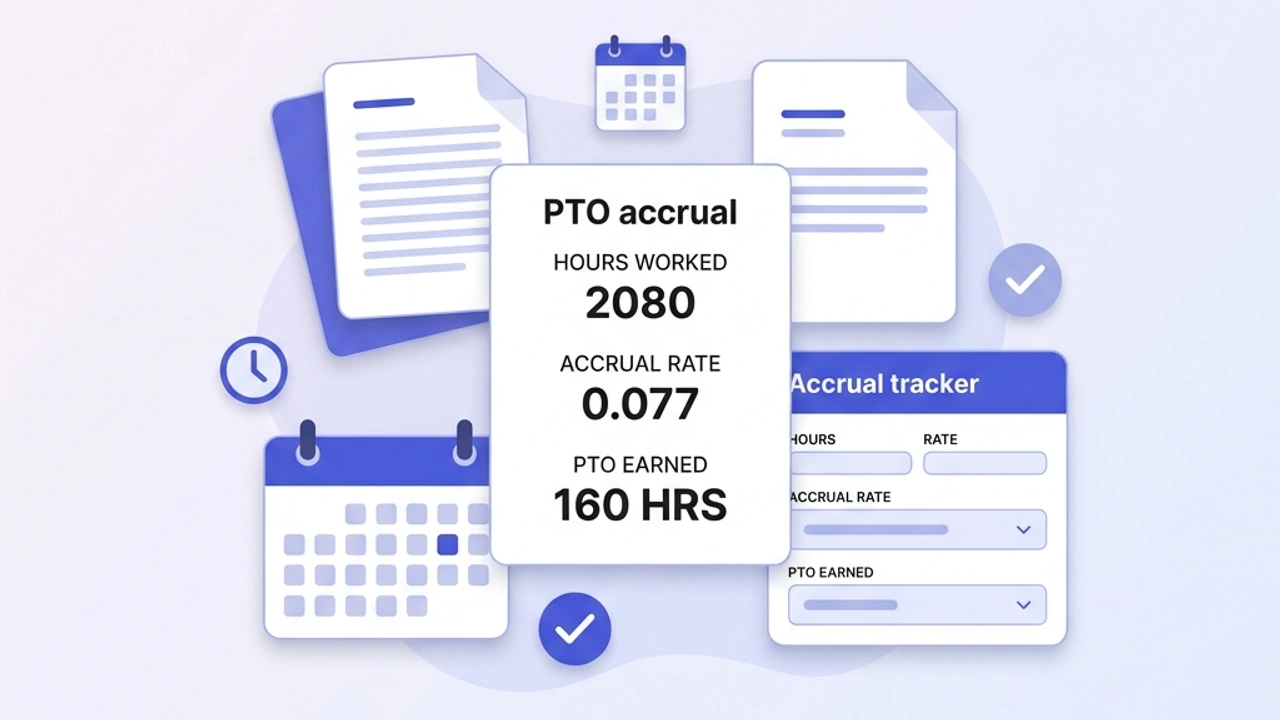

An employee is entitled to 15 days (120 hours) of PTO per year. They work full-time at 40 hours per week, totaling 2,080 hours annually.

Step 1 — Calculate the accrual rate:

Accrual Rate = 120 hours ÷ 2,080 hours = 0.0577 hours of PTO per hour worked

Step 2 — Calculate PTO earned in one biweekly pay period (80 hours worked):

PTO Earned = 0.0577 × 80 = 4.62 hours

Step 3 — Running balance after 3 pay periods:

Pay Period

Hours Worked

PTO Earned

Cumulative Balance

Period 1

80

4.62 hrs

4.62 hrs

Period 2

80

4.62 hrs

9.23 hrs

Period 3

72 (took 8 hrs PTO)

4.16 hrs

5.39 hrs

Notice in Period 3: the employee only worked 72 hours (they used 8 hours of PTO). Under strict hourly accrual, PTO does not accrue on PTO-taken hours — only on actual hours worked. Some employers choose to accrue on PTO hours as well; this must be explicitly stated in your policy.

Part-Time Accrual

The beauty of hourly accrual is that part-time employees are handled automatically. A part-time employee working 20 hours per week (1,040 hours/year) at the same 0.0577 rate would earn:

0.0577 × 1,040 = 60 hours (7.5 days) of PTO per year

This is exactly half the full-time allocation — perfectly proportional, and requiring no separate policy.

4. Method 2: Per-Pay-Period Accrual (Most Common)

Per-pay-period accrual is the most widely used method in payroll systems. Instead of tracking exact hours worked, a fixed amount of PTO is credited at the end of each pay period, regardless of minor variations in hours within that period.

The Formula:PTO Per Pay Period = Annual PTO Hours / Number of Pay Periods Per Year

Pay Period Frequencies and Accrual Rates

Pay Frequency

Pay Periods/Year

PTO Per Period (15 days/120 hrs)

PTO Per Period (20 days/160 hrs)

Weekly

52

2.31 hours

3.08 hours

Biweekly

26

4.62 hours

6.15 hours

Semi-monthly

24

5.00 hours

6.67 hours

Monthly

12

10.00 hours

13.33 hours

Step-by-Step Example

A full-time employee is entitled to 20 days (160 hours) of PTO per year. Payroll runs biweekly (26 pay periods per year).

Step 1 — Calculate PTO per pay period:

160 hours ÷ 26 = 6.15 hours per pay period

Step 2 — YTD balance at the end of Month 3 (6 pay periods):

6.15 × 6 = 36.92 hours (approximately 4.6 days)

Note on semi-monthly vs. biweekly: Semi-monthly payroll runs exactly 24 times per year (1st and 15th), while biweekly runs 26 times (every two weeks). In most years biweekly produces 26 periods, but occasionally produces 27 in a long year — your policy should specify how to handle this.

5. Method 3: Annual Lump-Sum Grant

While not technically "accrual," the annual lump-sum grant is common enough to deserve full coverage. Under this model, employees receive their full annual PTO allocation on a single defined date — either January 1st, or their individual work anniversary.

Pros:

Administratively simple — no running calculations required

Employees can plan holidays for the full year immediately

No partial-year accrual math when someone joins mid-year

Cons:

Creates 100% of the annual PTO liability on day one

If an employee uses all their PTO in January and then resigns, you may have difficulty recovering the "advance"

Requires a clear policy on what happens to unused balance at year-end

Mid-Year Hires Under Lump-Sum

If you use lump-sum grants, you still need a prorated calculation for employees hired after the grant date. The most common approach is to prorate based on months remaining in the year:

Prorated Grant = Annual PTO × (Months Remaining / 12)

An employee joining on September 1st with a 15-day annual entitlement receives:

15 days × (4 months remaining ÷ 12) = 5 days for the remainder of the year

6. Method 4: Tenure-Based Accrual Tiers

Many organizations incentivize loyalty by increasing the PTO accrual rate as employees accumulate tenure. This is one of the most powerful retention tools in HR — and it requires slightly more complex tracking.

Common Tenure-Based PTO Structure

Years of Service

Annual PTO Entitlement

Biweekly Accrual Rate

0 to 1 year

10 days (80 hours)

3.08 hours/period

1 to 3 years

15 days (120 hours)

4.62 hours/period

3 to 5 years

18 days (144 hours)

5.54 hours/period

5+ years

22 days (176 hours)

6.77 hours/period

Critical implementation note: When an employee crosses a tenure threshold (e.g., their 3-year anniversary), the new accrual rate applies to the next full pay period, not retroactively to the current period. Your payroll system or HR software should be configured to trigger the rate change automatically on the anniversary date.

Step-by-Step Example: Mid-Year Tier Change

An employee hits their 3-year anniversary on July 15th. Payroll is biweekly. They are moving from 4.62 hrs/period (15 days) to 5.54 hrs/period (18 days).

Pay periods 15–26 (Jul 15 – Dec 31): 5.54 × 12 = 66.48 hours accrued

Total for the year: 131.16 hours (blended between the two tiers)

This is correctly calculated — the employee does not earn the full 144-hour entitlement for a year in which they only crossed the threshold halfway through.

7. Accrual Caps: Why They Matter and How to Set Them

An accrual cap (sometimes called a "PTO ceiling" or "maximum balance") limits the total amount of PTO an employee can accumulate at any one time. Once an employee reaches the cap, they stop earning new PTO until they use some of their balance.

Why Caps Are Important for Employers

Without a cap, long-tenured employees who rarely take time off can accumulate enormous PTO balances. In jurisdictions where accrued PTO must be paid out at termination (which includes many US states, and most of the EU, UK, and Australia), these balances represent a growing, off-balance-sheet liability. A 10-year employee with 250 hours of unused PTO at a $45/hour salary represents a $11,250 termination liability — and that liability grows every year they continue working.

How to Set an Accrual Cap

The industry standard is to set the cap at 1.5× the annual PTO entitlement. This gives employees enough room to save up for a long vacation while preventing runaway balance accumulation.

📅

PTO Accrual Calculator

Model different cap scenarios and see exactly when an employee's balance will hit the ceiling based on their accrual rate.

Use-it-or-lose-it: Any unused PTO balance at year-end is forfeited. Simplest to administer, but illegal in many jurisdictions (including California, the EU, UK, and most of Australia). Before implementing this policy, confirm it is permitted under local employment law.

Full rollover: All unused PTO carries over to the next year. Creates uncapped liability risk if no maximum balance cap is set.

Capped rollover: The most common balanced approach. Unused PTO rolls over, but the total balance is capped at the maximum (e.g., 1.5× annual). Once the cap is hit, no new PTO accrues until the balance drops below the cap.

8. How to Handle PTO at Termination

The treatment of accrued, unused PTO at termination is one of the most legally sensitive areas of PTO policy, and it varies dramatically by jurisdiction.

Jurisdictions Where Payout Is Mandatory

United States: Varies by state. California, Colorado, Illinois, Massachusetts, and several others require full payout of accrued PTO at termination. Other states allow use-it-or-lose-it.

United Kingdom: All statutory annual leave must be paid out at termination. Employers cannot implement a "lose-it" policy for statutory leave entitlement.

European Union: Under the EU Working Time Directive, accrued holiday entitlement must be paid out upon termination. Individual member states may have additional requirements.

Australia: Under the National Employment Standards, employees are entitled to a payout of accrued annual leave at termination.

Canada: Federally regulated employees must receive vacation pay on termination; provincial rules vary.

For a salaried employee, convert to an hourly rate first:

Hourly Rate = Annual Salary / Annual Working Hours

A salaried employee earning $62,400/year ($30/hour at 2,080 hours) with 48 accrued hours at termination:

$30 × 48 = $1,440 termination PTO payout

This is why tracking accrual balances accurately throughout employment is so important — a small rounding error compounded over years can produce a meaningful discrepancy at the point of termination.

9. Building Your PTO Policy: A Step-by-Step Checklist

Before you can calculate anything, you need a defined policy. Use this checklist to ensure every decision is made before you implement:

✅ Entitlement Decisions

How many PTO days per year for each tenure tier?

Is PTO a single bank (covering holidays, sick, personal) or separate buckets?

Does PTO include public/bank holidays, or are those additional?

✅ Accrual Method

Hourly accrual, per-pay-period, or lump-sum grant?

Does PTO accrue during PTO-taken hours, or only during hours worked?

Does PTO accrue during unpaid leave, medical leave, or parental leave?

What is the waiting period for new hires (e.g., no accrual in first 90 days)?

✅ Balance Management

What is the maximum accrual cap?

Is unused PTO forfeited at year-end, or does it roll over?

If it rolls over, is there a cap on the rollover amount?

✅ Termination

Is accrued PTO paid out at termination? (Check local law — this may not be optional)

What is the calculation method for the payout?

Is the policy different for voluntary vs. involuntary termination?

✅ Administration

What payroll/HRIS system will track accrual balances?

How frequently are balances communicated to employees (each pay stub, monthly, on demand)?

Who is responsible for approving PTO requests and managing the schedule?

10. Common PTO Accrual Mistakes to Avoid

Failing to prorate for part-time employees. Using the same flat per-pay-period grant for both full-time and part-time workers overpays part-time staff. Always base accrual on hours worked or use a prorated annual entitlement.

Ignoring jurisdiction-specific mandatory minimums. In the UK, statutory minimum holiday entitlement is 28 days (including 8 bank holidays) for full-time workers. In the EU, the Working Time Directive mandates a minimum of 20 days. Many employers are unaware their policy falls below the legal minimum.

No waiting period policy for new hires. Without a defined waiting period, employees hired on January 2nd begin accruing immediately. This is fine if intentional, but many employers are surprised when a new hire quits after two months having already accrued 15 hours of PTO they now must be paid out.

Rounding errors that compound over time. When you round accrual rates (e.g., 4.62 vs. 4.615384...), small errors accumulate across 26 pay periods. Over a year, this can produce a balance that is 0.3 to 0.8 hours off from the intended entitlement. Use 4 decimal places in your accrual rate to minimize drift.

Not auditing balances annually. Run an annual reconciliation comparing accrued hours per employee against the theoretical entitlement for their tenure. Discrepancies caught early are simple data corrections; discrepancies caught at termination become legal disputes.

Final Thoughts on PTO Administration

A well-designed PTO accrual system is invisible to employees — balances simply appear on their pay stubs, and they trust the numbers are correct. A poorly designed one generates HR tickets, manager disputes, and legal exposure every time an employee leaves the company.

The foundation of a good system is a clear, documented policy and an accurate calculation method that is applied consistently. Start with the method that matches your payroll frequency and workforce composition, define your caps and rollover rules in writing, and verify compliance with the employment laws in every jurisdiction where you employ people.

📅

Free PTO Accrual Calculator

Plug in your accrual rate, hours worked, and pay frequency to instantly calculate accrued balances, project year-end totals, and estimate termination payouts for any employee.

Divide your employee's total annual PTO allowance by the number of pay periods in the year. For example, if they get 120 hours of PTO and you run payroll bi-weekly (26 periods), they accrue 4.62 hours per pay period.

Does PTO accrue on overtime hours?

Generally, no. Most companies calculate PTO accrual based on standard working hours (typically 40 hours per week). Overtime hours do not generate additional PTO unless explicitly stated in your company's policy or union agreement.

What is an accrual cap?

An accrual cap is the maximum amount of PTO an employee can bank at any given time. Once they reach the cap (e.g., 1.5x their annual allowance), they stop accruing additional hours until they take time off.

Is use-it-or-lose-it legal for PTO?

It depends on local labor laws. In some US states like California, earned PTO is considered wages and cannot be taken away (use-it-or-lose-it is illegal). Always consult local employment laws when designing your rollover policy.

How is PTO paid out upon termination?

If you are legally required to pay out accrued PTO, multiply the employee's accrued hours by their normal hourly wage. For salaried employees, divide their annual salary by 2080 (standard full-time working hours) to find their hourly rate.

#how to calculate PTO accrual#paid time off accrual#vacation accrual rate#HR policy#employee benefits#accrual cap