How to Calculate Compound Interest for Business Savings

Learn how to calculate compound interest for business savings accounts, reserve funds, and reinvestment strategies. Includes formulas, tables, and worked examples.

BT

Bizcalc Team

·June 15, 2026

Every dollar sitting idle in a non-interest-bearing business account is a dollar that is not working for you. For small and medium-sized businesses, understanding how compound interest works — and actively leveraging it — can meaningfully grow reserve funds, emergency buffers, tax provisions, and retained earnings over time, without any additional revenue being generated.

Yet compound interest remains one of the most underused tools in business financial management. Most business owners understand it conceptually but have never applied the formula to their own numbers to see what it actually means for their cash reserves over one, three, or five years.

This guide explains the compound interest formula in plain terms, walks through worked examples using business-relevant scenarios, compares compounding frequencies, and gives you a practical framework for deciding where and how to deploy compound interest in your business finances.

📈

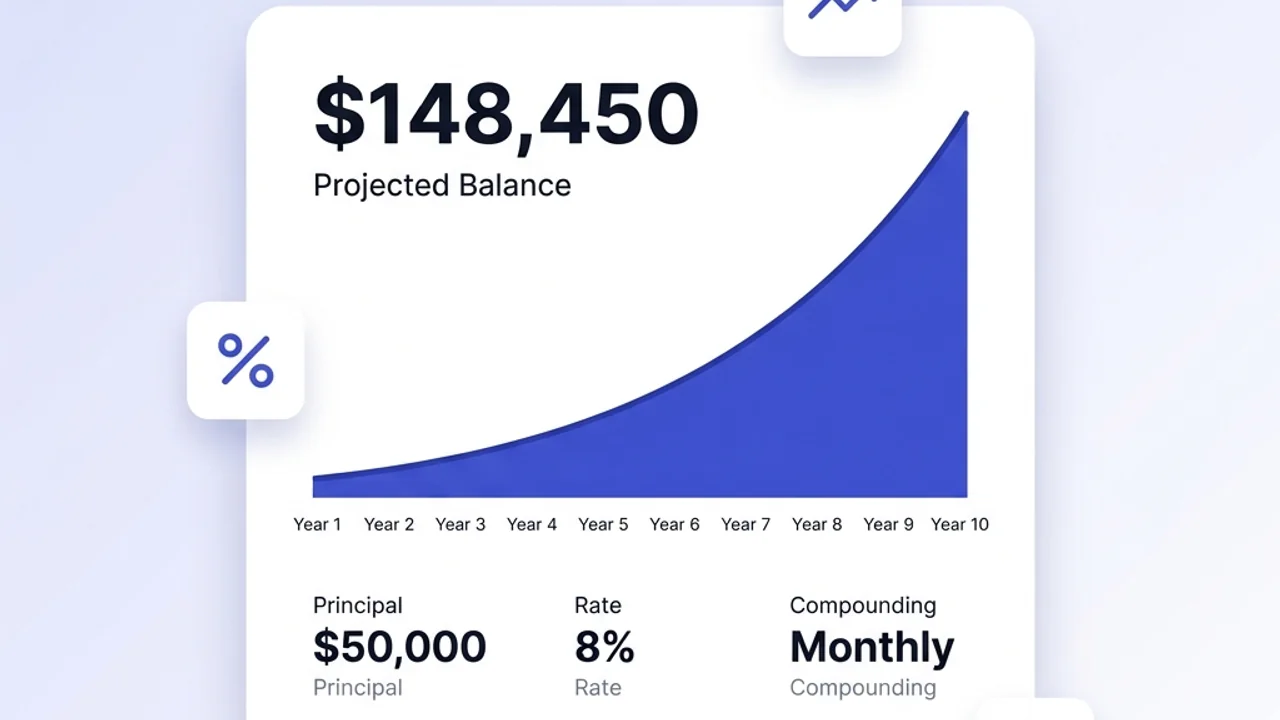

Compound Interest Calculator

Enter your principal, interest rate, and compounding frequency to instantly see how your business savings will grow over time.

Compound interest is interest calculated on both the initial principal and the accumulated interest from previous periods. In contrast to simple interest — which is calculated only on the original principal — compound interest causes a balance to grow at an accelerating rate because each period's interest payment itself earns interest in subsequent periods.

This is the mechanism behind what Albert Einstein reportedly called "the eighth wonder of the world." Whether or not that attribution is accurate, the mathematics is undeniably powerful: a business that consistently places its idle cash into a compounding vehicle rather than leaving it in a zero-interest account will accumulate significantly more over the medium and long term.

Simple Interest vs. Compound Interest: A Quick Comparison

Consider $50,000 held for 5 years at a 6% annual interest rate:

Method

Year 1

Year 2

Year 3

Year 4

Year 5

Total Interest Earned

Simple Interest

$3,000

$3,000

$3,000

$3,000

$3,000

$15,000

Compound Interest (annual)

$3,000

$3,180

$3,371

$3,573

$3,788

$16,912

With annual compounding at the same rate, the business earns an additional $1,912 compared to simple interest — entirely from interest compounding on itself. Extend this to 10 years and the gap widens dramatically.

The Compound Interest Formula

The standard formula for compound interest is:

A = P(1 + r/n)^(nt)

Where:

A = Final amount (principal + total interest earned)

P = Principal (the initial deposit or starting balance)

r = Annual interest rate expressed as a decimal (e.g., 5% = 0.05)

n = Number of compounding periods per year (e.g., 12 for monthly, 4 for quarterly, 365 for daily)

t = Time in years

To find only the interest earned (not the total balance), subtract the principal:

Interest Earned = A − P

Understanding the Compounding Frequency Variable (n)

The compounding frequency determines how often earned interest is added to your balance and begins earning interest of its own:

Compounding Frequency

Value of n

Annually

1

Semi-annually

2

Quarterly

4

Monthly

12

Daily

365

The higher the value of n, the more frequently interest compounds and the slightly higher the effective return. For most practical business savings scenarios, the difference between monthly and daily compounding is marginal — but the difference between annual and monthly compounding on large balances over multiple years can be meaningful.

Step-by-Step: How to Calculate Compound Interest for Business Savings

Step 1: Identify Your Principal (P)

This is the lump sum you are depositing or the current balance in the account. For a business, this might be:

Retained earnings set aside for future investment

A tax reserve fund awaiting a quarterly or annual payment

An emergency operating reserve

Revenue from a contract or sale being held before deployment

Step 2: Confirm the Annual Interest Rate (r)

Obtain the exact interest rate from your bank or financial institution. Convert the percentage to a decimal by dividing by 100. A rate of 4.75% becomes r = 0.0475.

Always confirm whether the rate quoted is the APR (Annual Percentage Rate) or the APY (Annual Percentage Yield). APR is the base rate; APY already accounts for compounding and represents the true annual return. When comparing accounts, always use APY.

Step 3: Determine the Compounding Frequency (n)

Check your account's terms. Most high-yield business savings accounts and money market accounts compound daily (n = 365) or monthly (n = 12). Standard business current accounts typically pay no interest at all.

Step 4: Define Your Time Horizon (t)

Express the time in years. Six months = 0.5, eighteen months = 1.5, three years = 3, and so on.

Step 5: Apply the Formula

Substitute your values into A = P(1 + r/n)^(nt) and calculate.

Step 6: Subtract Principal to Find Interest Earned

Interest Earned = A − P

Worked Examples for Business Scenarios

Example 1: Tax Reserve Fund

A business sets aside $30,000 in a high-yield savings account earning 4.8% APR, compounding monthly (n = 12), for 9 months (t = 0.75 years).

That is over $1,100 earned on money that was simply sitting in reserve waiting to pay a tax bill — at no additional effort or risk.

Example 2: Business Emergency Fund Over 3 Years

A business builds an emergency operating reserve of $75,000 and places it in a money market account earning 5.1% APR, compounding daily (n = 365), for 3 years.

Over three years, the business earns more than $12,000 in passive interest on its emergency fund — without touching the principal. This effectively reduces the real cost of maintaining an operating reserve.

Example 3: Retained Earnings Reinvestment

A profitable small business retains $120,000 in earnings after its year-end close and places the full amount in a short-term business savings account at 4.5% APR, compounding quarterly (n = 4), while the owners decide how to deploy the capital over 18 months (t = 1.5).

The business earns $8,359 simply by placing its retained earnings in a compounding savings vehicle instead of leaving them in a standard current account while decisions are made.

Comparison Summary: All Three Examples

Scenario

Principal

Rate

Frequency

Term

Interest Earned

Tax Reserve

$30,000

4.8%

Monthly

9 months

$1,101.60

Emergency Fund

$75,000

5.1%

Daily

3 years

$12,137.25

Retained Earnings

$120,000

4.5%

Quarterly

18 months

$8,359.20

📈

Compound Interest Calculator

Model any of these scenarios with your own figures — adjust principal, rate, frequency, and term to see your projected business savings balance instantly.

How Compounding Frequency Affects Business Returns

To illustrate the real-world impact of compounding frequency, consider $100,000 earning 5% annual interest over 5 years under different compounding schedules:

Compounding Frequency

Final Balance

Total Interest Earned

Annually (n = 1)

$127,628.16

$27,628.16

Quarterly (n = 4)

$128,203.24

$28,203.24

Monthly (n = 12)

$128,335.87

$28,335.87

Daily (n = 365)

$128,400.34

$28,400.34

The difference between annual and daily compounding on $100,000 over 5 years is $772.18 — meaningful but not dramatic. What matters far more than compounding frequency is the interest rate itself and the length of time the money is invested.

Key takeaway: When choosing a business savings vehicle, prioritize the highest available APY over the compounding frequency. A monthly-compounding account at 5.2% will always outperform a daily-compounding account at 4.9%.

The Effect of Time: Why Early Saving Compounds Fastest

The most powerful variable in the compound interest formula is time (t). The longer a sum compounds, the more pronounced the exponential growth effect becomes.

Consider a business that deposits $50,000 at 5% annual interest, compounding monthly, and leaves it untouched:

Year

Balance

Interest Earned That Year

1

$52,558.70

$2,558.70

2

$55,247.72

$2,689.02

3

$58,074.92

$2,827.20

4

$61,047.69

$2,972.77

5

$64,174.99

$3,127.30

7

$71,069.13

—

10

$82,378.95

—

15

$105,752.73

—

20

$135,797.25

—

Notice that the interest earned in Year 5 ($3,127) is 22% higher than in Year 1 ($2,559) — not because the rate changed, but purely because the balance has grown. By Year 20, the original $50,000 has grown to over $135,000 — a 171% increase — entirely from compounding.

This illustrates why businesses that establish long-term savings habits (for capital expenditure funds, succession planning, or expansion reserves) benefit disproportionately from starting early.

APY vs. APR: The Metric That Actually Matters for Business Accounts

When evaluating business savings options, the Annual Percentage Yield (APY) is the definitive comparison metric. APY already incorporates the effect of compounding, making it an apples-to-apples comparison across accounts with different compounding frequencies.

APY Formula:

APY = (1 + r/n)^n − 1

Example: An account advertises a 5.0% APR compounding monthly.

So while the headline rate is 5.0%, the money in this account actually grows at an effective rate of 5.116% per year once monthly compounding is applied.

If a competing account offers 5.05% APR but compounds only quarterly:

APY = (1 + 0.0505/4)^4 − 1 = 5.14%

Despite the lower APR, the quarterly-compounding account actually produces a slightly higher APY. Always compare APY figures when evaluating business savings accounts.

Where Businesses Can Apply Compound Interest

Understanding the compound interest formula is most useful when it is applied to real decisions about how a business manages its cash. Here are the primary business contexts where compounding creates measurable value:

1. Tax Reserve Accounts

Most businesses should maintain a dedicated reserve for VAT, GST, corporation tax, payroll tax, or quarterly estimated tax payments. Rather than holding these funds in a zero-interest current account, placing them in a high-yield savings account for the weeks or months before they are due generates passive interest income on money that would otherwise sit idle.

2. Emergency Operating Funds

Financial planning best practice recommends that businesses maintain 3–6 months of operating expenses as an emergency reserve. This is often a substantial sum — for a business with $50,000 in monthly expenses, the recommended reserve is $150,000–$300,000. Placing this in a compounding savings vehicle rather than a standard current account is a straightforward, low-risk way to generate returns on an otherwise static balance.

3. Sinking Funds for Capital Expenditure

If a business anticipates a large future expenditure — a facility upgrade, equipment replacement, fleet expansion, or technology investment — a disciplined savings plan with compound interest dramatically reduces the amount that needs to be set aside each month to reach the target. The Savings Goal Calculator can help you calculate exactly how much to deposit monthly to reach a specific target by a defined date.

4. Retained Earnings Parking

Between major business decisions — an acquisition, a partnership buyout, a significant hiring round — retained earnings often sit in cash for months or quarters. Placing these funds in a short-term compounding savings account while decisions are finalized is a no-cost improvement over leaving them in a non-interest-bearing account.

5. Business Investment Accounts

Beyond traditional savings accounts, businesses with a longer time horizon can apply compound interest principles to investment portfolios, where dividend reinvestment and capital gains compounding over 5–10+ year periods can generate substantially larger returns than short-term cash savings. The Net Present Value Calculator is useful for evaluating whether the compounding return on a savings strategy meets your business's required rate of return relative to other capital deployment options.

Compound Interest vs. Loan Interest: The Other Side of the Equation

Compound interest works both for and against businesses. While it grows savings, it also accelerates debt when applied to loans, credit facilities, or unpaid balances.

A business credit line charging 18% APR compounding monthly on an unpaid $20,000 balance generates:

That same $20,000 earning 5% APY in savings generates only ~$1,025 in the same period. The asymmetry is stark: compound interest on business debt typically accrues at rates 3–5 times higher than on business savings.

The practical implication: before prioritizing savings, businesses should evaluate whether eliminating high-interest debt delivers a higher guaranteed return than any available savings rate. The Loan Payment Calculator can help model total interest costs on existing debt obligations.

Building a Business Compound Interest Strategy: A Checklist

Use this checklist to systematically apply compound interest to your business cash management:

Audit all current accounts — identify balances sitting in zero-interest current accounts and quantify the opportunity cost.

Open a dedicated high-yield business savings account — separate from your operating account to prevent co-mingling and accidental spending.

Calculate your optimal reserve size — use your monthly operating expenses to determine the appropriate emergency fund balance (typically 3–6 months of expenses).

Set up a tax reserve sub-account — automatically transfer a percentage of revenue into a compounding savings account designated for upcoming tax obligations.

Compare APY figures — when evaluating savings products, always compare APY (not APR) to ensure you are seeing the true effective annual return.

Define time horizons for each reserve — short-term reserves (under 12 months) suit liquid savings accounts; medium-term reserves (1–5 years) may suit notice accounts or term deposits with higher rates.

Review rates quarterly — interest rate environments change. Review your savings account rates each quarter and move funds if materially better options become available.

Model future balances before making decisions — before deciding how long to hold retained earnings in cash, calculate the compound interest that balance will earn to factor it into your total return picture.

Common Mistakes Businesses Make with Compound Interest

Mistake 1: Leaving Large Balances in Zero-Interest Accounts

The most prevalent and costly mistake. Many businesses maintain six- or seven-figure balances in standard current accounts purely out of habit. A $200,000 balance earning 0% instead of 5% APY costs the business approximately $10,000 in foregone interest per year.

Mistake 2: Comparing APR Instead of APY

Choosing a savings account based on its APR without converting to APY can lead to selecting a lower-yielding product. Always compare the effective annual return, not the nominal rate.

Mistake 3: Prioritizing Savings Over High-Interest Debt

If a business carries high-interest revolving credit at 15–20% while earning 5% on savings, the net position is a guaranteed loss. Eliminating the debt first delivers a risk-free return equal to the debt's interest rate — almost always higher than any available savings rate.

Mistake 4: Underestimating the Power of Regular Contributions

The examples above all assume a single lump-sum deposit. In reality, businesses that make regular monthly contributions to a savings account benefit from both compound interest and dollar-cost averaging. Even modest monthly additions dramatically accelerate balance growth over time.

Mistake 5: Ignoring Inflation-Adjusted Returns

A 5% savings return in a 3% inflation environment produces a real return of approximately 2%. For long-term reserves, ensure that the nominal interest rate is meaningfully above the prevailing inflation rate to preserve purchasing power.

Final Thoughts

Compound interest is not a complex concept — but its power in a business context is consistently underestimated. Every business holds cash: in reserves, in tax provisions, in retained earnings, in sinking funds. The difference between actively managing that cash in compounding vehicles and passively leaving it in a standard account can amount to tens of thousands of dollars over a few years — with zero additional risk.

The first step is simply to run the numbers. Once you can see in concrete dollar terms what your idle cash reserves could be earning, the case for action becomes obvious.

🎯

Savings Goal Calculator

Set a target balance, enter your starting amount and interest rate, and instantly calculate the monthly deposit required to reach your business savings goal.

What is the compound interest formula for business savings?

The standard compound interest formula is A = P(1 + r/n)^(nt), where A is the final amount, P is the principal, r is the annual interest rate (as a decimal), n is the number of compounding periods per year, and t is the number of years. The more frequently interest compounds, the faster the balance grows.

How is compound interest different from simple interest?

Simple interest is calculated only on the original principal each period. Compound interest is calculated on the principal plus all previously earned interest, so your returns grow exponentially over time. For long-term business savings, the difference between the two can be substantial.

How often does compound interest compound?

Common compounding frequencies are daily, monthly, quarterly, and annually. Most high-yield business savings accounts and money market accounts compound daily or monthly. The more frequent the compounding, the slightly higher the effective return — though the difference between daily and monthly compounding is usually small in practice.

What is APY and how does it differ from APR for business savings?

APR (Annual Percentage Rate) is the stated interest rate before compounding effects. APY (Annual Percentage Yield) reflects the true annual return after compounding is applied. When comparing business savings accounts, always compare APY figures rather than APR, as APY is the accurate measure of what your balance will actually grow to in a year.

Can a business use compound interest to grow a tax reserve or emergency fund?

Yes — placing tax reserves, emergency funds, or retained earnings into a high-yield business savings account or money market account allows those funds to earn compound interest while they sit idle. Even at modest rates, compounding over 6–24 months adds measurable value and ensures the money is working rather than sitting in a non-interest-bearing current account.

#compound interest calculation for business#compound interest formula#business savings#interest compounding#business finance